Greetings,

It’s the

SEASON OF FESTIVALS and of course, the season for the Women's Best friend, GOLD!! WE INDIANS LOVE GOLD!

Gold is very close to women and has a huge sentimental value and

an emotional attachment.

One of the

most popular ways of buying Gold

which even a common middle-class family is looking for is a GOLD CHIT FUND.

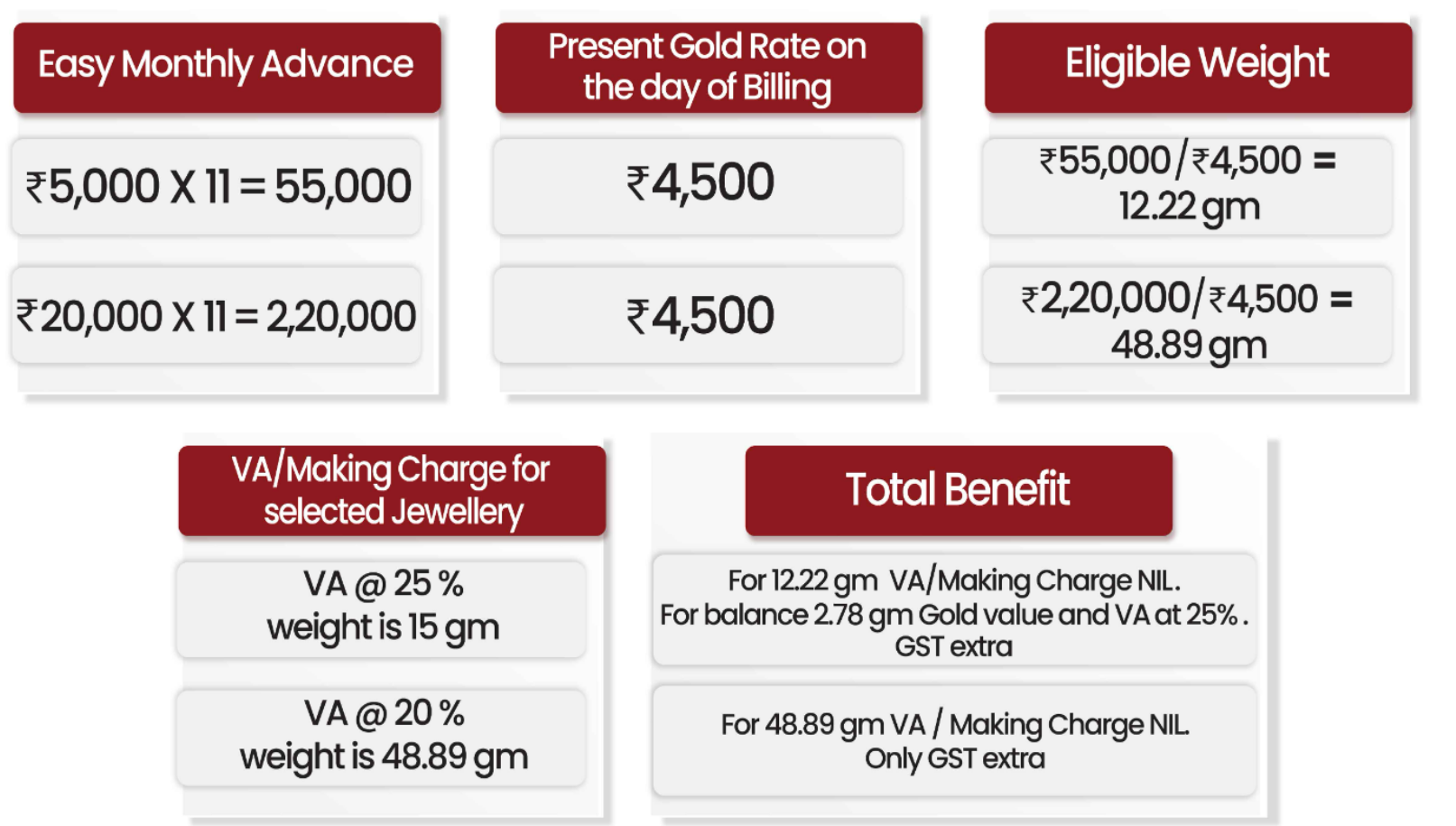

Under this Gold Chit fund, you need

to pay a Fixed Sum of amount for 11 months and at the end of the 11th month,

you are given the 12th-month instalment FREE by the Jeweller and as a Bonus

offering, many also offer you Gold Jewellery with ZERO WASTAGE CHARGES.

In short,

these schemes are EMI in Reverse. They help you buy Jewellery at a Future date

by saving and accumulating.

The

brochures show returns ranging from 10% to as high as 24% per annum.

Does sound

good. Isn’t it?

Or is it?

Let’s find

out...

SOME OF

THE MOST POPULAR GOLD CHIT SCHEMES ARE

Tanishq Gold Harvest Scheme

GRT Golden Eleven Flexi Scheme

Bhima Gold Tree Purchase Plan

Kalyan Dhan Samriddhi Scheme

PROs:

1. Discount

on Wastage. In fact, some jewellers offer ZERO WASTAGE CHARGES (Sadly, these

ZERO wastages is only for a few select designs and for good intricate designs, the jeweller could still slam a higher levy).

2. Allows a

simple effective way of accumulating large sums of money needed for Gold Purchase (like a

monthly SIP in mutual funds)

CONS:

1. These

schemes do not have any Regulation and thus if the Jeweller goes bankrupt, your

money is GONE!

2. You HAVE

to compulsorily buy Jewellery even if the Jeweller does not have designs of

your liking and also you will have to pay Making charges, etc.

The designs

may not be of your liking but you are now STUCK

3. The Gold Savings scheme by

Jewellers does not have SEBI approval and thus there is no monitoring of the cash you

pay. These Jewellers may be using your fund for Working Capital, business, etc

and nobody checks their books. So, if tomorrow, suddenly Gold price crashes and

all Investors stop their instalments and ask for Gold, then you never know how many of these

Jewellers would be able to keep their word.

4. Very few

Jewellers offer 24 Karat Gold.

Almost every jeweller offers only 22k gold. So, since you will not get cash from the

Jeweller, you are buying Gold

which is not 100% pure.

5. If at the

end of the Instalment period, you are in need of Cash for an emergency, you won’t

be able to use this money as you are given only Jewellery. The best you can do

is to sell the piece of Jewellery and forgo the making charges.

NOTABLE

POINT:

Some

Jewellers offer the choice of blocking grams of Gold when each monthly instalment is paid or the

normal method of Amount Accumulation.

At the time

of Maturity (redemption), you can choose which route works best for you (grams

or amount route)

Our view is

that:

In times of

Rising Gold prices,

grams work better and in times of Falling Gold prices, the amount accumulated works best.

ALSO, KEEP IN MIND:

Some

jewellers like GRT do allow the purchase of GOLD COINS.

These

schemes make sense only if you have a PLANNED jewellery purchase which matches

the Maturity Month of the scheme. If you don’t have any plans to buy jewellery, don’t

even look at these schemes.

And also,

you can go ahead and subscribe to this Gold Chit fund only if you are comfortable with

the fact that you have to buy Jewellery only from that particular shop.

MOST

IMPORTANT:

If you do

decide to go ahead with taking a Gold Chit, make sure you go with reputed Jewellers as many

Fly-By-Night Operators have vanished after collecting crores of rupees (VGN

Jewellers, etc)

Jewellers

like Tanishq, and GRT have a good

reputation.

And of

course, as we always keep saying, GOLD IS NOT FOR RETURNS. There are many better options for

Investments which are superior to Gold when it comes to Returns.

You can also

consider other options like the Gold Mutual Funds and the best of them all namely SGB.

SGB is Sovereign

Gold Bonds. SGB gives 2.5% interest with a 5-year lock-in period.

And SGB is

backed by 24k Pure Gold.

But, Sir, the 12th-month

instalment is FREE. What about that?

Well,

Jewellers are not here for charity, they give FREE last instalment with money

made from your previous instalments!

Jewellers

not only earn interest on the buyer's instalment but also sell the jewellery

after earning a handsome margin. For 20 grams of gold jewellery, he earns Rs 600 making charge and

sells 22-carat gold

at a rate of 24 carat gold.

So, he earns approx. 8% extra by selling gold of 22-carat purity.

For jewellers,

this scheme is a win-win situation as he gets the chance to sell their product,

and at the same time, he earns interest on the customer’s instalment.

For lower middle-class

people, and for people who want to accumulate Gold for marriage or other purposes in near

future, the Jeweller Gold

Saving Scheme looks okay, but for all other purposes, the SOVERIGN GOLD BOND by the

Government of India is the BEST.

THE BIGGEST ATTRACTION

for me is that this SGB gives me Interest of 2.5% every year (on base value)

and mirrors the prices of the Market Value of Gold.

Neither Gold Chit Funds, Physical

Gold, Gold Mutual Funds or Gold ETFs pay any

Interest.

For a Gold

lover, SGB is a GOD-SENT WINDOW to invest in Gold (especially as it is GST-free too!!)

If you are

hell-bent on investing in these schemes of Jewellers, then I feel that Tanishq

and GRT are better

among the Worst.

ANOTHER

POINT TO NOTE:

Most

investors invest in Bank Recurring Deposits to buy Gold at a future date. This is not a good

idea since Interest Rates may not keep pace with the rise in Gold prices and they will

not be able to achieve their objective.

FINAL WORD:

Gold Jewellery Schemes aim to give you Gold/Jewellery whereas gold Savings Funds/Gold ETFs aim to give you

Cash.

So, if you

want to buy Jewellery in the near future (say 1 year), then go for Jewellery Gold Savings Schemes, but

if you want to buy Gold

as an Investment or if your Gold

usage is at a later date (say your daughter's marriage, which is several years

away), then it's Gold

Savings Fund/Gold

ETF blindly.

The caveat, if

it is for consumption, then unless you have a very trusted and reliable

Jeweller (ready to buy back from you), don’t think of these Gold Savings Schemes by

Jewellery Stores.

Buy Gold ETF, Sell the Units

when you want gold and from the money you get, go buy gold!

SPECIAL

TIP ONLY FOR OUR READERS:

If you do

have a Gold Chit

fund, when you go to the Jeweller at the time of maturity (redemption) DO NOT

reveal that you have a Gold

Chit scheme, first select the Jewellery you want, get the estimated Bill and

only after this REVEAL that you have a Gold Scheme!!

All the Very

Best,

Srikanth

Matrubai

Author: DON’T

RETIRE RICH

&

WEALTH OF

WISDOM (WOW)

All the best,

Regards,

Srikanth Matrubai

https://t.me/joinchat/AAAAAELl4KUnaJzi-JJlDg/